What Is Stripe in 2026: New Features Quietly Changing How Ecommerce Businesses Get Paid

16 April 2026

Anna P.

13 minutes

Stripe is a payment processor — but that description undersells what it's become for ecommerce businesses. Businesses running on Stripe generated $1.9 trillion in total payment volume in 2025, up 34% from 2024, equivalent to roughly 1.6% of global GDP. It now powers 90% of the Dow Jones Industrial Average and 80% of the Nasdaq 100. (Stripe) In February 2026, Stripe was valued at $159 billion — approximately a 70% increase from its $91.5 billion valuation in February 2025. (TechCrunch)

For ecommerce store owners, Stripe is the infrastructure that makes accepting payments online possible without building banking relationships from scratch, handling PCI compliance manually, or connecting directly to major credit card networks. It sits between your online store and your customer's bank account — processing the transaction, handling fraud detection, managing payouts, and doing all of it invisibly while you focus on selling.

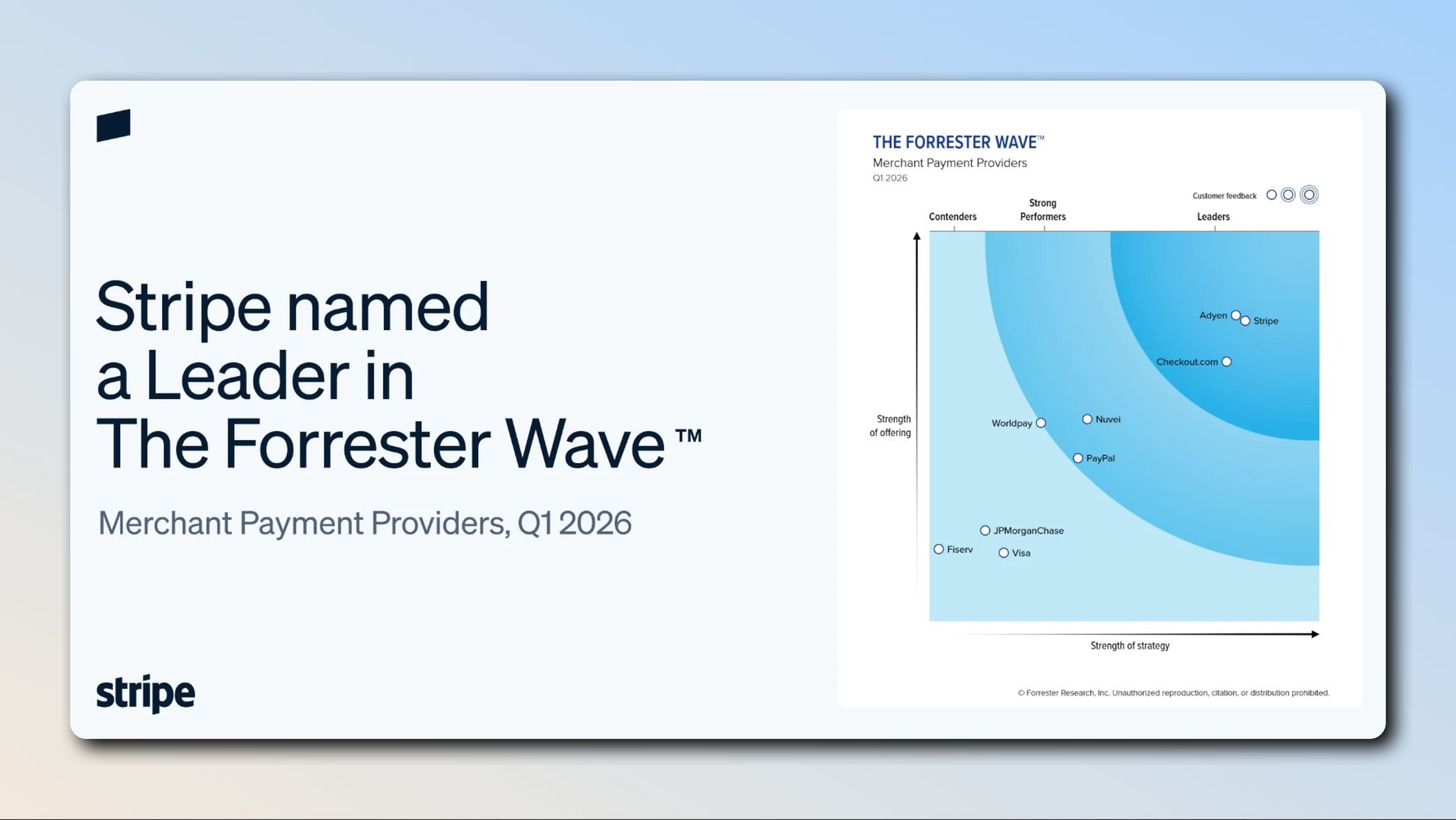

Stripe has been named a Leader in The Forrester Wave: Merchant Payment Providers, Q1 2026, recognized for its vision, innovation, ease of use, and speed to value for businesses of all sizes.

This guide covers what Stripe does, which features matter most for how ecommerce accepts payments, what it costs, and what's changed in Q1 2026 that affects online businesses.

How Stripe Processes Online Payments

When a customer enters their credit card details at your checkout, Stripe handles every step to process payments:

authenticating the card

routing the transaction through the relevant credit card networks (Visa, Mastercard, American Express, Discover)

communicating with the customer's bank account

receiving approval or decline

depositing the net amount into your business bank account (typically within two business days)

What separates Stripe from older payment processors is how much control ecommerce store owners have over the experience. The Stripe dashboard gives you a complete real-time view of every transaction, refund, and dispute — plus the Stripe data and advanced reporting through Stripe Sigma to make informed decisions about payment performance, authorization rates, and revenue.

Stripe now handles bank debits including ACH and SEPA direct debit, digital wallets including Apple Pay and Google Pay, buy now pay later schemes like Klarna, and stablecoin payments — making it one of the broadest payment method options available to online businesses through a single integration.

Stripe Features That Matter Most for Ecommerce

Not every Stripe feature carries equal weight for an ecommerce business. The ones below have the most direct impact on conversion rates, revenue per order, fraud protection, and international reach — in roughly that order of immediate relevance to store owners running paid traffic.

Stripe Optimized Checkout Suite — Biggest Revenue-Driver for Merchants

The Optimized Checkout Suite is Stripe's most significant product for ecommerce conversion and the one with the most documented revenue impact. It's a pre-built, hosted checkout experience with dynamic payment method display, one-click checkout via Link, BNPL options, and local payment methods — all managed by Stripe rather than configured manually by the merchant.

The updated Stripe Payment Element within the Optimized Checkout Suite supports 34 payment methods including alternative and local payment methods, ACH vaulting for repeat customers to save bank details for faster future checkouts, dynamic payment method sorting that automatically prioritizes the most relevant options for each shopper, and A/B testing of local payment methods to identify which options drive the highest conversions.

For online retailers, this is significant: payment method display order affects completion rates, and dynamic sorting that adapts to each customer's context — location, device, prior payment behavior — produces better results than a fixed payment method list.

Read more: Shopify Checkout Optimization

Stripe Link — One-Click Checkout for Returning Customers

Link is Stripe's one-click checkout that autofills payment information for customers who have saved their details with any Stripe-powered store. Once a customer's credit card details are stored in Link — which happens automatically when they check out through any participating merchant — they can complete future purchases across any Stripe-powered checkout with a single click and a phone verification code.

Businesses with large repeat customer bases have seen an average returning user conversion increase of 14% with Link enabled. Link enables customers to check out 3x faster than non-Link customers, and the network reaches over 200 million consumers worldwide. (Stripe)

Link autofills customers' payment information, which can drive up conversion rates by over 7% for logged-in users. (Stripe)

For online stores where repeat purchases are a meaningful revenue driver — subscriptions, consumables, apparel, anything with a natural replenishment cycle — Link's network effect compounds over time as more customers have their details stored. Each returning customer who sees their information pre-filled is a customer who doesn't have to re-enter credit card payment details at your checkout.

The updated Link experience places the quick payment button at the top of checkout — ensuring the fastest path to purchase — and now supports Instant Bank Payments, giving shoppers more flexible ways to pay instantly.

Stripe Radar — AI Fraud Prevention That Protects Revenue

Stripe Radar is the fraud prevention layer that runs on every transaction. It uses a machine learning system trained on data from millions of Stripe merchants globally to assign a risk score to each payment and block fraudulent transactions before they complete.

Stripe Radar leverages machine learning to reduce fraud by 38% on average. (Stripe) Stripe's AI foundation model for payments, trained on tens of billions of transactions, has already improved detection of sophisticated card testing attacks by 64% compared to its previous systems. (Stripe)

Card testing — where fraudsters run small transactions to verify stolen card numbers before using them for larger purchases — is one of the most damaging fraud patterns for ecommerce stores because it generates chargebacks, elevated dispute rates, and potential account risk. The AI model improvement on this specific attack type is directly relevant to any store that has experienced unusual transaction patterns or unexpected chargeback spikes.

Radar runs automatically on every transaction with no additional setup. The base version applies Stripe's default risk rules. Radar for Fraud Teams is the paid upgrade at $0.02 per transaction that adds custom rule-building and manual review workflows for stores with specific fraud patterns requiring more granular control.

Stripe Terminal — In-Person Transactions for Ecommerce Brands

For businesses that also sell at pop-up events, trade shows, or physical retail locations, Stripe Terminal extends the same payment infrastructure to in-person transactions. You can accept in-person payments via contactless payments, chip cards, and mobile wallets through Stripe-compatible card readers — with every transaction visible in the same Stripe dashboard as your online payments.

In-person transactions through Stripe Terminal run at a lower rate than online card payments: 2.7% + $0.05 per transaction for in-person cards and wallets, compared to 2.9% + $0.30 online. If you're running events or market stalls where margins are tight, the cost difference is meaningful at volume.

Stripe Billing — Recurring Payments and Subscription Management

Stripe Billing handles recurring payments, subscription management, trials, upgrades, downgrades, and dunning — automated failed payment recovery — for ecommerce businesses building subscription models. Stripe Billing now has more than 300,000 users and was recognized as a Leader in both the 2025 Gartner Magic Quadrant for Recurring Billing Applications and The Forrester Wave: Recurring Billing Solutions for Q1 2025. (Stripe)

For retailers adding subscription options to physical products — replenishment subscriptions, curated box services, membership programs — Stripe Billing handles the complexity of recurring charge scheduling, failed payment retries, and customer portal access without custom development.

Stripe International Payments and Multi-Currency Support

Stripe supports over 135 currencies and handles currency conversion automatically. If you're selling internationally, this means a customer in Germany paying in euros gets the same checkout experience as a domestic customer — with automatic currency display and conversion.

Stripe has rolled out multicurrency balance capabilities, allowing businesses to hold and manage funds in USD, EUR, and GBP within a single Stripe account — enabling international merchants to avoid foreign exchange fees by transacting and storing money in local currencies.

For stores with significant European revenue, holding euros in a Stripe account and spending in euros on European ad platforms, suppliers, or operations eliminates the conversion fee on every transaction — a cost that compounds significantly at scale.

Stripe Connect — Manage Payments for Marketplaces and Platforms

If you're operating as a marketplace — where multiple sellers fulfill orders through your platform — Stripe Connect manages payment routing, fee splitting, and payout distribution automatically. Each seller has their own Stripe account managed through your platform, and Connect handles the regulatory and compliance complexity of moving money between multiple parties without requiring custom payment infrastructure.

How Much Does Stripe Cost: What You Pay Per Transaction

Stripe operates on a pay-as-you-go model with no setup fees and no monthly fees on the standard plan. The standard US rate is 2.9% + 30¢ per successful online card transaction — on a $100 sale, you pay $3.20 and receive $96.80.

Additional fees apply in specific situations: manually keyed card transactions carry 3.4% + 30¢; international card transactions add 1.5%; in-person transactions via Stripe Terminal run at 2.7% + $0.05; ACH direct debit charges 0.8%, capped at $5 per transaction.

Disputed charges cost $15 per chargeback, win or lose. If you have high dispute volumes, Stripe's Chargeback Protection add-on covers both the disputed amount and the dispute fee.

For high-volume merchants processing $100,000+ per month, Stripe offers custom enterprise pricing through direct negotiation — rates as low as 2.2% + 30¢ have been reported at sufficient volume.

What's New in Stripe Q1 2026: Updates Ecommerce Merchants Need to Know

Q1 2026 has been Stripe's most active quarter for product and infrastructure announcements in recent memory. The updates below are the ones with direct implications for ecommerce merchants — not developer tooling or enterprise features, but changes that affect conversion rates, cross-border costs, and fraud protection at the store level.

Stripe Named Leader in Forrester Wave Q1 2026

Stripe was named a Leader in The Forrester Wave: Merchant Payment Providers, Q1 2026 — recognized for vision, innovation, ease of use, and speed to value across business sizes. (Stripe) When evaluating payment infrastructure, this is the most credible third-party validation of Stripe's position in the payments industry and a signal that its direction — AI-driven conversion tools, stablecoin infrastructure, agentic commerce — is being validated externally, not just marketed internally.

Stripe Optimized Checkout Suite Now Expanding to More Platforms

In January 2026, BigCommerce announced a significant expansion of its Stripe partnership, giving merchants worldwide access to Stripe's Optimized Checkout Suite — including dynamic local payment methods, BNPL, and AI-driven fraud prevention tools. The pattern is consistent across platforms: Stripe is pushing its Optimized Checkout Suite as a conversion tool, not just payment infrastructure.

Ecommerce businesses using Stripe directly via API or through a Stripe-integrated funnel builder benefit from the same capabilities without waiting for platform-level rollouts.

Stripe Stablecoin Volume Quadrupling — Cross-Border Payments Getting Cheaper

Bridge, the stablecoin platform Stripe acquired in 2024, saw transaction volume more than quadruple in 2025. (CoinDesk) In February 2026, Stripe's annual letter confirmed that stablecoin volume is decoupling from crypto market cycles as real-world payment use expands.

If you manage heavy international sales, this matters practically. Cross-border card transactions carry additional fees — 1.5% for international cards, 1% for currency conversion — that stablecoin payment rails reduce significantly. As Stripe continues developing its stablecoin infrastructure through Bridge and the Tempo blockchain it is co-building with Paradigm, international payment costs for ecommerce are likely to decrease over the next 12–24 months.

In January 2026, Stripe acquired the team behind Valora, a mobile crypto wallet startup, to accelerate stablecoin payment capabilities with consumer-friendly mobile interfaces. (CoinDesk) This signals stablecoin payments are moving toward mainstream consumer checkout — not just developer tooling.

Stripe AI Payments Model Improving Authorization Rates

Stripe's AI foundation model for payments — trained on tens of billions of transactions — is improving not just fraud detection but authorization rates across the board. False declines are one of the most underappreciated revenue leaks in ecommerce: a legitimate customer's card gets declined because a risk model incorrectly flagged it, the customer doesn't realize their card wasn't the problem, and the sale is lost permanently. Stripe's AI model is trained specifically to reduce this, meaning more legitimate transactions complete on the first attempt.

For ecommerce stores running high-volume paid traffic, authorization rate improvements compound across every campaign. A 1–2% improvement in authorization rate on 10,000 monthly transactions is 100–200 additional completed orders with no additional ad spend.

Stripe Multicurrency Balances — Keeping International Revenue in Local Currency

Launched in early 2026, multicurrency balance accounts let ecommerce businesses hold USD, EUR, and GBP within a single Stripe account without converting between them on every transaction. This enables international merchants to avoid foreign exchange fees by transacting and storing money in local currencies.

In practice: a UK-based D2C brand running Meta ads in Europe can now receive euro revenue, hold it as euros, and spend it on European suppliers or ad platforms without triggering a currency conversion fee at each step. For stores where international revenue is a meaningful share of total sales, this is a quietly significant cost reduction that compounds across every international order.

How Stripe and Funnelish Work Together for Ecommerce

Stripe is the payment infrastructure. What it doesn't do is optimize the checkout experience for conversion — the design, flow, and friction level of the checkout page itself is a separate layer that determines how many customers who arrive actually complete the purchase.

Funnelish integrates Stripe natively as one of its payment gateway options alongside PayPal, Klarna, iDEAL, SEPA, and more — giving customers every payment method option they expect, with Stripe handling the processing backend while Funnelish handles the experience that converts intent into payment. The checkout flow is designed for paid traffic conversion: one-page checkout, all express payment options visible, trust signals placed at the moments that reduce payment anxiety.

Post-purchase one-click upsells use the payment details captured by Stripe in the original transaction to process additional purchases with a single tap — no re-entering credit and debit card details, no new checkout flow. Every order syncs automatically to Shopify or WooCommerce. Stripe's fraud prevention runs on every transaction, including upsells. The combination of Stripe's payment reliability and Funnelish's conversion-optimized checkout is what makes the unit economics of paid traffic work at scale.

Start your free 14-day Funnelish trial →

Stripe FAQs

Is Stripe the same as PayPal?

No. Both are payment processors but they work differently. Stripe is developer-first infrastructure designed to integrate into your own checkout flow — you control the entire customer experience and Stripe handles the payment processing behind it. PayPal has its own recognized checkout interface that customers interact with directly. Many ecommerce stores use both: Stripe for card payments through a custom checkout and PayPal as an additional payment method for customers who prefer it.

What exactly does Stripe do?

Stripe is the infrastructure between your online store and your customer's bank account. When a customer pays, Stripe authenticates their card, routes the transaction through the relevant credit card networks, communicates with the customer's bank to approve or decline, runs fraud detection through its machine learning system, and deposits the net amount to your business bank account.

It also manages recurring payments, international payments, refunds, disputes, and provides the Stripe dashboard for monitoring all payment activity.

How much is the Stripe fee for $100?

On a standard $100 domestic card transaction in the US, Stripe charges 2.9% + $0.30, totaling $3.20. You receive $96.80. International card transactions add 1.5%, and currency conversion adds another 1% — a $100 payment from an international customer paying in a foreign currency costs up to $5.20 in total fees.

Is Stripe legitimate and safe?

Yes. Stripe maintains PCI service provider level 1 compliance — the highest security certification in the payments industry. It serves companies from solo founders to Amazon and Shopify, and processes nearly $2 trillion in annual payment volume. Its fraud prevention runs automatically on every transaction.

Is Stripe safe to link a bank account?

Yes. Stripe uses bank-level encryption to connect to your business bank account for payouts. The connection is used only to receive funds — Stripe cannot initiate withdrawals. Every payout is fully visible in the Stripe dashboard before it reaches your bank account.

What are the risks of using Stripe?

The main operational risk is account holds — Stripe can hold funds if it detects unusual activity or high dispute rates, sometimes without immediate explanation. This is standard across payment processors. At scale, a business processing $50,000/month pays roughly $1,480 in Stripe fees, and additional costs from chargebacks, international card surcharges, and premium add-ons add up faster than the base rate suggests. Managing dispute rates through Radar and reliable fulfillment is the most effective risk mitigation.

What banks connect to Stripe?

Stripe connects to virtually any business bank account for payouts — all major US banks including Chase, Bank of America, Wells Fargo, and Citibank, as well as online banks like Mercury, Relay, and Brex that are popular with ecommerce businesses. For instant payouts, Stripe requires a supported debit card linked to the account.

Table of contents

Boost your eCommerce

sales today

24/7 support

No credit card required

Cancel anytime

24/7 support

No credit card required

Cancel anytime